Introduction to Difference in Differences

ECON526

University of British Columbia

Introduction

Introduction

- Context:

- Have a policy applied to some observations but not others, and observe outcome before and after policy

- Idea:

- Compare outcome before and after policy in treated and untreated group

- Change in outcome in treated group reflects both effect of policy and time trend, change in untreated group captures time trend

Example: Impact of Billboards

- From Facure (2022) chapter 13

- Bank placed billboards advertising savings accounts in Porto Alegre in July

- Data on deposits in May and July in Porto Alegre and Florianopolis

Example: Impact of Billboards

Means and Differences

| deposits | ||

|---|---|---|

| poa | 0 | 1 |

| jul | ||

| 0 | 171.642308 | 46.01600 |

| 1 | 206.165500 | 87.06375 |

Difference in Differences

\[ % \def\Er{{\mathrm{E}}} \def\En{{\mathbb{E}_n}} \def\cov{{\mathrm{Cov}}} \def\var{{\mathrm{Var}}} \def\R{{\mathbb{R}}} \newcommand\norm[1]{\left\lVert#1\right\rVert} \def\rank{{\mathrm{rank}}} \newcommand{\inpr}{ \overset{p^*_{\scriptscriptstyle n}}{\longrightarrow}} \def\inprob{{\,{\buildrel p \over \rightarrow}\,}} \def\indist{\,{\buildrel d \over \rightarrow}\,} \DeclareMathOperator*{\plim}{plim} \]

Setup

- Two periods, binary treatment in second period

- Potential outcomes \(\{y_{it}(0),y_{it}(1)\}_{t=0}^1\) for \(i=1,...,N\)

- Treatment \(D_{it} \in \{0,1\}\),

- \(D_{i0} = 0\) \(\forall i\)

- \(D_{i1} = 1\) for some, \(0\) for others

- Observe \(y_{it} = y_{it}(0)(1-D_{it}) + D_{it} y_{it}(1)\)

Identification

- Average treatment effect on the treated:

\[ % \begin{align*} ATT & = \Er[y_{i1}(1) - \color{red}{y_{i1}(0)} | D_{i1} = 1] \\ & = \Er[y_{i1}(1) - y_{i0}(0) | D_{i1} = 1] - \Er[\color{red}{y_{i1}(0)} - y_{i0}(0) | D_{i1}=1] \\ & \text{ assume } \Er[\color{red}{y_{i1}(0)} - y_{i0}(0) | D_{i1}=1] = \Er[y_{i1}(0) - y_{i0}(0) | D_{i1}=0] \\ & = \Er[y_{i1}(1) - y_{i0}(0) | D_{i1} = 1] - \Er[y_{i1}(0) - y_{i0}(0) | D_{i1}=0] \\ & = \Er[y_{i1} - y_{i0} | D_{i1}=1, D_{i0}=0] - \Er[y_{i1} - y_{i0} | D_{i1}=0, D_{i0}=0] \end{align*} \]

Important Assumptions

- No anticipation: \(D_{i1}=1\) does not affect \(y_{i0}\)

- built into the potential outcomes notation we used

- could relax by allowing potential outcomes given sequence of \(D\), i.e. \(y_{it}(D_{i0},D_{i1})\), but then need different assumptions and estimator

- Parallel trends: \(\Er[\color{red}{y_{i1}(0)} - y_{i0}(0) |D_{i1}=1,D_{i0}=0] = \Er[y_{i1}(0) - y_{i0}(0) | D_{i1}=0, D_{i0}=0]\)

- not invariant to tranformations of \(y\)

Estimation

Plugin: \[ % \widehat{ATT} = \frac{ \sum_{i=1}^n (y_{i1} - y_{i0})D_{i1}(1-D_{i0})}{\sum_{i=1}^n D_{i1}(1-D_{i0})} - \frac{ \sum_{i=1}^n (y_{i1} - y_{i0})(1-D_{i1})(1-D_{i0})}{\sum_{i=1}^n (1-D_{i1})(1-D_{i0})} \]

Regression: \[ % y_{it} = \delta_t + \alpha 1\{D_{i1}=1\} + \beta D_{it} + \epsilon_{it} \] then \(\hat{\beta} = \widehat{ATT}\)

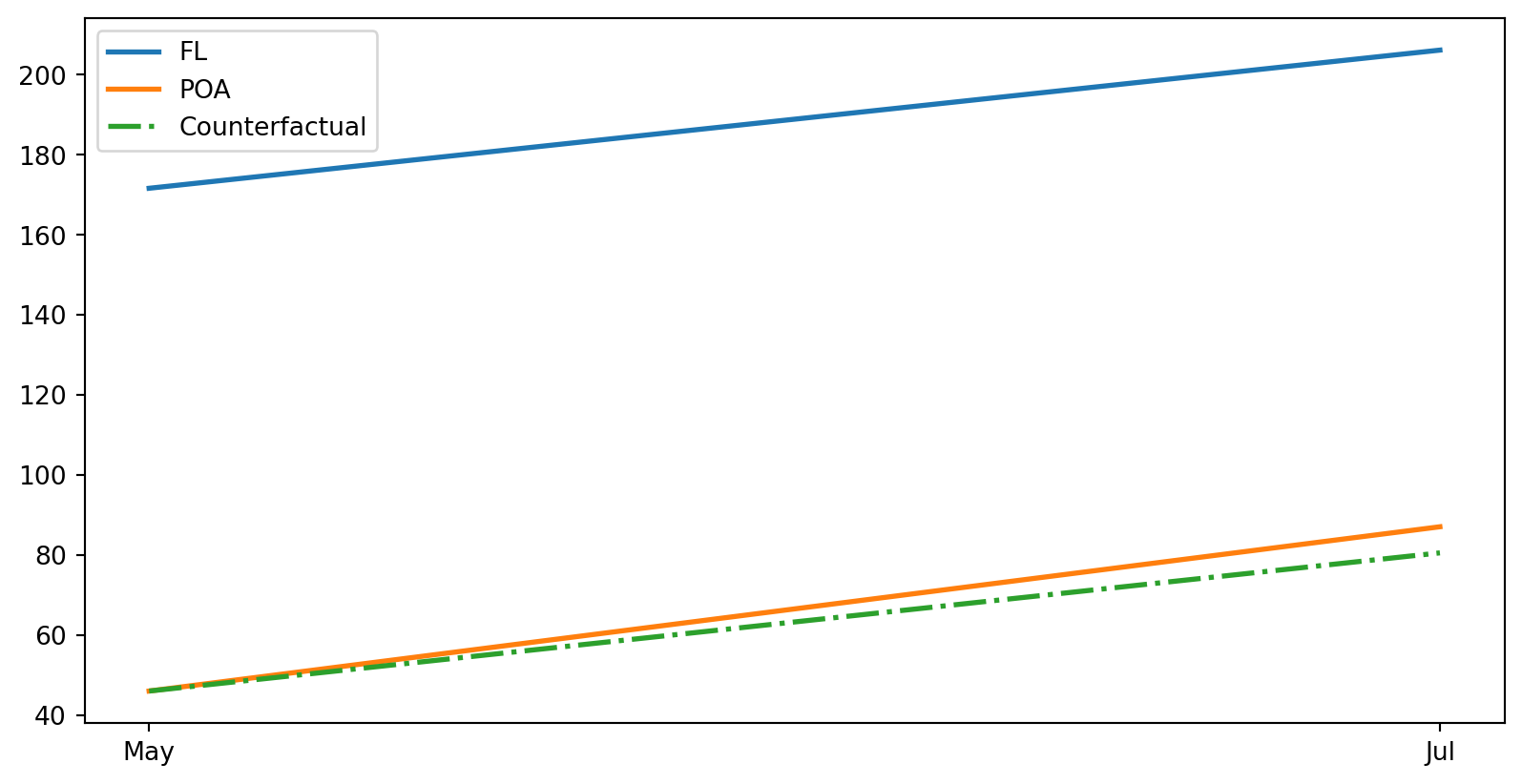

Billboard Application Revisited

Visualizing Difference in Differences

poa_before = data.query("poa==1 & jul==0")["deposits"].mean()

poa_after = data.query("poa==1 & jul==1")["deposits"].mean()

fl_before = data.query("poa==0 & jul==0")["deposits"].mean()

fl_after = data.query("poa==0 & jul==1")["deposits"].mean()

plt.figure(figsize=(10,5))

plt.plot(["May", "Jul"], [fl_before, fl_after], label="FL", lw=2)

plt.plot(["May", "Jul"], [poa_before, poa_after], label="POA", lw=2)

plt.plot(["May", "Jul"], [poa_before, poa_before+(fl_after-fl_before)],

label="Counterfactual", lw=2, color="C2", ls="-.")

plt.legend();

Estimation via Regression

| deposits | |

|---|---|

| Intercept | 171.6423 |

| (2.4989) | |

| poa | -125.6263 |

| (3.0774) | |

| jul | 34.5232 |

| (3.3431) | |

| poa:jul | 6.5246 |

| (4.2478) | |

| R-squared | 0.3126 |

| R-squared Adj. | 0.3122 |

Standard errors in parentheses.

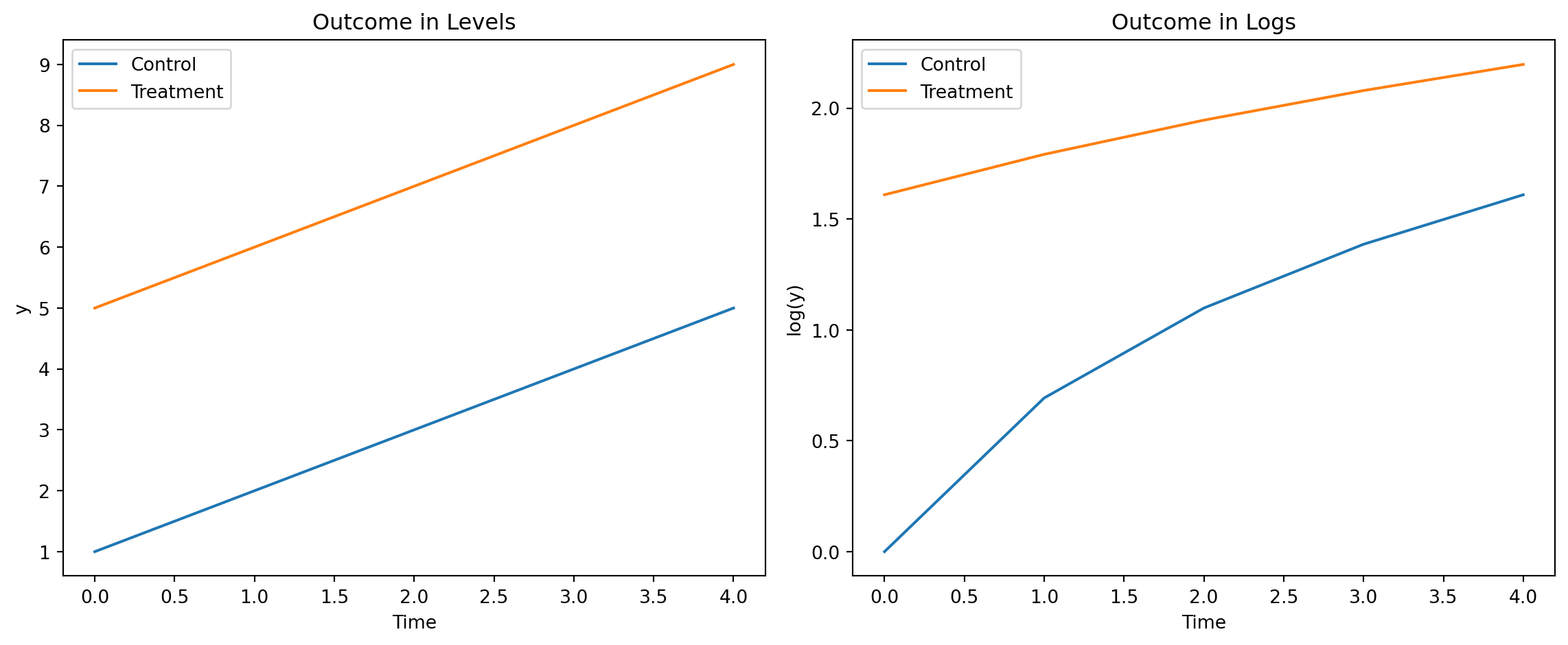

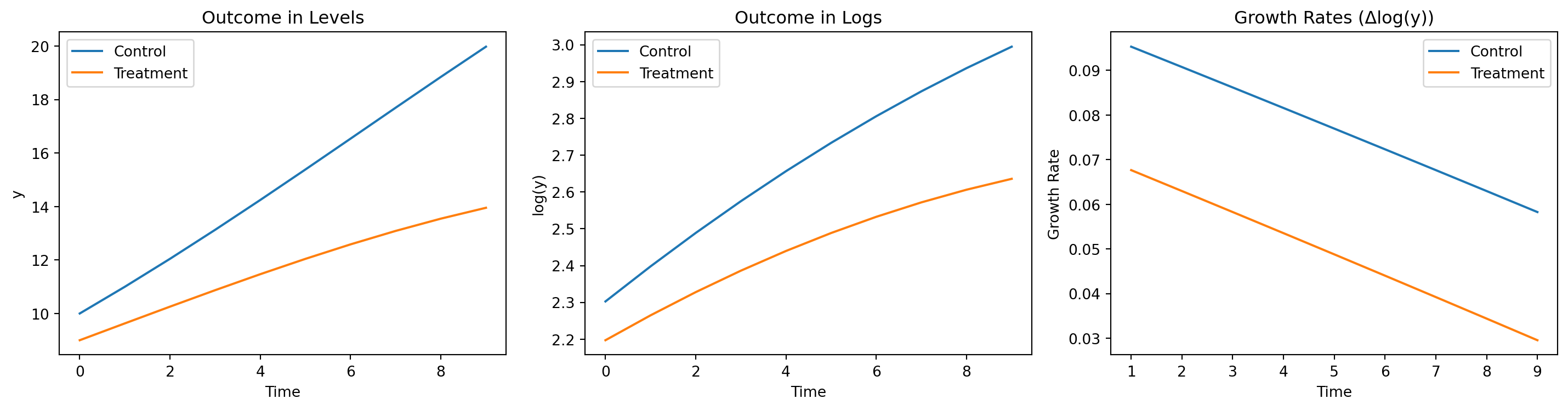

Parallel Trends and Functional Form

- Parallel trends for an outcome does not imply parallel trends for functions of it

- For example, \[ \Er[\color{red}{y_{i1}(0)} - y_{i0}(0) |D_{i1}=1,D_{i0}=0] = \Er[y_{i1}(0) - y_{i0}(0) | D_{i1}=0, D_{i0}=0] \] does not imply \[ \Er[\log \color{red}{y_{i1}(0)} - \log y_{i0}(0) |D_{i1}=1,D_{i0}=0] = \Er[\log y_{i1}(0) - \log y_{i0}(0) | D_{i1}=0, D_{i0}=0] \]

Parallel Trends in Logs

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

# Parameters

n_periods = 5

n_groups = 2

group_names = ['Control', 'Treatment']

time = np.arange(n_periods)

group = np.array([0, 1]) # 0: Control, 1: Treatment

intercepts = [1, 5] # Different starting points

trend = 1 # Same trend for both groups

# Simulate outcomes

data = []

for g in group:

for t in time:

y = intercepts[g] + trend * t #+ np.random.normal(0,1)

data.append({'group': group_names[g], 'time': t, 'y': y})

df = pd.DataFrame(data)

df['log_y'] = np.log(df['y'])

# Plot levels

plt.figure(figsize=(12,5))

plt.subplot(1,2,1)

for name, grp in df.groupby('group'):

plt.plot(grp['time'], grp['y'], label=name)

plt.title('Outcome in Levels')

plt.xlabel('Time')

plt.ylabel('y')

plt.legend()

# Plot logs

plt.subplot(1,2,2)

for name, grp in df.groupby('group'):

plt.plot(grp['time'], grp['log_y'], label=name)

plt.title('Outcome in Logs')

plt.xlabel('Time')

plt.ylabel('log(y)')

plt.legend()

plt.tight_layout()

plt.show()Parallel Trends in Logs

Parallel Trends in Growth Rates

# Parameters

n_periods = 10

group_names = ['Control', 'Treatment']

initials = [10, 9] # Different starting values

growth = [1.10, 1.07]

growth_trend = -0.005

# Simulate outcomes

data = []

for g, initial in enumerate(initials):

y = initials[g]

for t in range(n_periods):

data.append({'group': group_names[g], 'time': t, 'y': y})

y *= growth[g] + growth_trend * t

df = pd.DataFrame(data)

df['log_y'] = np.log(df['y'])

# Compute growth rates (difference in logs)

df['growth_rate'] = df.groupby('group')['log_y'].diff()

# Plot levels

plt.figure(figsize=(15,4))

plt.subplot(1,3,1)

for name, grp in df.groupby('group'):

plt.plot(grp['time'], grp['y'], label=name)

plt.title('Outcome in Levels')

plt.xlabel('Time')

plt.ylabel('y')

plt.legend()

# Plot logs

plt.subplot(1,3,2)

for name, grp in df.groupby('group'):

plt.plot(grp['time'], grp['log_y'], label=name)

plt.title('Outcome in Logs')

plt.xlabel('Time')

plt.ylabel('log(y)')

plt.legend()

# Plot growth rates

plt.subplot(1,3,3)

for name, grp in df.groupby('group'):

plt.plot(grp['time'], grp['growth_rate'], label=name)

plt.title('Growth Rates (Δlog(y))')

plt.xlabel('Time')

plt.ylabel('Growth Rate')

plt.legend()

plt.tight_layout()

plt.show()Parallel Trends in Growth Rates

Further Topics

- More periods, more groups

- Covariates

- Pre-trends

Reading

- Chapter 13 of Facure (2022)